Frequently Asked Questions for Nursery Value Select

Nursery Value Select NVS

Editors Note: Please find the most up-to-date Frequently Asked Questions on Nursery Value Select (NVS) on the RMA website here.

Nursery Value Select (NVS) is a pilot crop insurance program that functions as an asset-based form of insurance coverage. In its pilot phase, it will run concurrent to the current nursery crop insurance program that is currently available.

Q. Where is Nursery Value Select NVS crop insurance available?

NVS is available in select counties in Alabama, Colorado, Florida, Michigan, New Jersey, Oregon, Tennessee, Texas, and Washington. Refer to the actuarial documents to determine if NVS is available in your county: webapp.rma.usda.gov/apps/actuarialinformationbrowser/.

Q. When will NVS be available?

NVS is available beginning with the 2021 crop year. For Alabama, Florida, New Jersey and Texas, the sales closing date is May 1, 2020 for the 2021 crop year. The crop year for those states begins June 1, 2020 and ends on May 31, 2021. For all other pilot states and counties, the sales closing date is September 1, 2020. The crop year for those states begins on October 1, 2020 and ends on September 30, 2021.

Q. Why should I purchase NVS?

The goal of NVS was to develop a nursery crop insurance program that addresses concerns expressed by stakeholders regarding the current nursery crop insurance program: participation is declining, nursery producers and agents remain concerned with onerous paperwork requirements, and the costs of maintaining required materials to support underwriting the program continue to be burdensome. NVS addresses these shortcomings by offering the following benefits:

- Simplification of the application and annual policy renewal process;

- Allowing nursery producers to select the dollar amount of coverage that best fits their risk management needs, and for buy-up policies; coverage tailored by an individual practice (container or field grown) or by choosing from any of 10 potential plant categories;

- A simplified loss adjustment process that uses a more accurate approach to determining plant values by placing greater reliance upon the nursery producer’s actual sales receipts, along with increased producer participation in determining a damaged plant’s ability to be marketed or rehabilitated;

- Elimination of a plant list based on third-party software and greater reliance on the producer’s inventory records, along with plant category naming conventions more familiar to the nursery industry;

- Tailored program dates, including two sales closing dates of May 1 (Alabama, Florida, New Jersey, and Texas) or September 1 (remaining pilot states) that are better suited to the agronomic and industry nursery management practices in different regions across the country; and

- A new Occurrence Loss Option (OLO) moving the deductible from a unit level to a plant level for an additional premium (only available for buy up policies).

Q. What are the eligibility requirements?

In order to be eligible for NVS coverage, you must be a wholesale nursery that derives at least 40 percent of its gross income from the wholesale marketing of plants to:

- Retailers who resell to end users;

- Landscape contractors;

- Government entities or organizations; and/or

- Commercial fruit producers.

You must also have a wholesale catalog that is provided to customers and used in the sale of the plants.

Q. What documentation do I need to provide to my crop insurance agent in order to obtain NVS insurance?

You must submit the following:

- Crop insurance application;

- Nursery Value Report (NVR) for each insured practice (field grown and/or container grown).

- The NVR is a document that represents your declaration of the insurance choices you elect.

- Monthly Unit Value Report (MUVP) for each insured basic unit.

- The MUVP is a document that represents your declaration for each basic unit by:

- Month, from the first month to the last month of the insurance period; and

- By the maximum value of all specific plants in each insured plant category that you expect to have in your nursery (during each month of the insurance period.)

- The MUVP is a document that represents your declaration for each basic unit by:

- Submit two printed copies or one electronic copy of the most recent catalog or price list, by season or plant category, if appropriate.

All documents must be acceptable and must be submitted on or before the sales closing date, except the MUVP*, for insurance to attach on the first day of the insurance period.

*If you are a carryover insured, you may certify on your NVR in subsequent years that there were no material changes to your previously-submitted MUVP and, therefore, an updated MUVP would not be required to be submitted.

Q. What is the deadline to submit the required documentation?

For insurance to attach on the start date of the crop year, all documentation must be submitted on or before the sales closing date.

- For new and first-year insureds, if you’re applying for coverage after the sales closing date:

- Insurance does not attach until the 31st day (30-day waiting period) after acceptable documents are filed; and

- Premium is owed from the first day of the month insurance attaches.

- For carryover insureds, all documentation must be submitted on or before the sales closing date in order to have coverage for the upcoming crop year.

Q. What unit structures are available under NVS?

Basic units are the only unit structure available under NVS. A basic unit consists of the following:

- All insurable plants;

- All insured plant categories; and

- Each practice that you elect to insure.

Basic units may be further divided by the following:

- For additional coverage:

- Each plant category you elect to insure; and

- Non-contiguous land, for field grown practice only.

- For catastrophic (CAT) coverage, further division of the basic unit is not allowed.

An administrative fee is due for each insured plant category if additional coverage is elected, and for each insured practice if CAT coverage is elected.

Q. Must I insure all my nursery plants under NVS?

No. Whether you have the catastrophic level of coverage or additional levels of coverage, NVS allows you to insure your field grown practice, your container grown practice or both. Additionally, for additional levels of coverage only, NVS allows you to choose which plant categories within the insured practice you wish you to insure. Once you have selected the plant categories you wish to insure, all plants within those plant categories must be insured.

Q. The current nursery crop insurance program has a plant list. Does NVS have a plant list?

No, NVS does not use a plant list. Under the current nursery program, using third-party software, each plant is assigned to a plant type, a cold protection requirement and hardiness zones where the plant can be insured. NVS’s structure does not require the use of this software. Instead, plant categories were created and defined in such a way that a plant list was not needed. These plant categories vary slightly from the insurable plant types under the current nursery program but are named in such a way that is familiar to producers. Each plant category’s definition contains a list of genera to assist producers in grouping their plants for insurance purposes. The insurable plant categories are as follows:

- Liners

- Annual Plants and Plants Grown for One Year or Less

- Herbaceous Biennial and Perennial Plants

- Foliage Plants

- Vines

- Deciduous Trees and Shrubs

- Broadleaf Evergreen Trees and Shrubs

- Coniferous Trees and Shrubs

- Palms

- Cycads

Cold protection requirements may still be needed for container grown plants if cold protection is identified by plant category in the Special Provisions.

Q. What is the insured crop?

The insured crop will be all the plants within each insured practice for CAT coverage, and each plant category you choose to insure within each insured practice for additional coverage and that:

- You have a share;

- Are determined by the insurance company to be acceptable;

- Are grown in a county for which a premium rate is provided in the actuarial documents;

- Are grown in a nursery determined by us to be acceptable;

- Are irrigated unless otherwise provided by the Special Provisions (you must have adequate irrigation equipment and water to irrigate all insurable nursery plants at the time coverage attaches and throughout the insurance period);

- Are grown in accordance with the production practices for which premium rates have been established;

- Are grown in an appropriate medium;

- Are grown and sold with the root system attached;

- Are not grown solely as stock plants or plants being grown solely for harvest of buds, flowers, or greenery;

- May produce edible fruits or nuts provided the plants are made available for sale (harvest of the edible fruit or nuts does not affect insurability);

- For the field grown practice, must be adapted in the hardiness zone recognized by the USDA Plant Hardiness Zone Map in which they are grown;

- For the container grown practice, are individual plants grown in standard nursery containers unless otherwise permitted by the Special Provisions;

- Were not damaged in a prior crop year unless such specific plants have been rehabilitated and are offered for sale at the approved sales value for the current crop year;

- Are not any plant classified by a state or county as illegal to grow or sell in the county in which the nursery is located; and

- Are not produced in nursery containers that contain two or more different genera, species, subspecies, varieties or cultivars, unless otherwise provided in the Special Provisions.

Q. The 2018 Farm Bill allowed for coverage of industrial hemp in the Federal crop insurance program. Is industrial hemp insurable under NVS?

Yes, but with some restrictions. In accordance with sections 8(h) and (i) of the NVS Crop Provisions, industrial hemp (Cannabis sativa L.), as defined in the Agricultural Marketing Act of 1946 (7 U.S.C. 1621 et seq.), is insurable when grown and sold with the root system attached in containers and are not stock plants or plants being grown solely for harvest of buds, flowers, or greenery.

- You must comply with all applicable Federal regulations and any applicable state or tribal laws.

- Regardless of state or tribal law, the sale of hemp with a THC level greater than 0.3 percent will be considered the sale of a controlled substance. Controlled substances are not insurable.

- If you produce industrial hemp in a state or tribal territory which has assumed regulatory responsibility for hemp production, you must comply with all requirements and provisions of the regulatory plan of that state or tribe and possess any license required by that plan. You must provide a copy of your license by the sales closing date.

- Industrial hemp must be produced using seed or plant cuttings adapted and appropriate for the intended use (for example, if planting industrial hemp to be harvested primarily for fiber, the seed must be adapted to fiber production). Industrial hemp that is unsalable or destroyed due to a delta-9 tetrahydrocannabinol (THC) level that exceeds 0.3 percent will be considered damaged due to uninsurable causes.

Q. How is my amount of insurance determined?

Amount of insurance is calculated by multiplying the coverage level you elect by the Selected Value (SV). The SV is the value you declare on your NVR of the insurable specific plants in each insured plant category.

- For additional coverage:

- The SV may not exceed the highest maximum value for the same plant category reported on your MUVP;

- If you do not elect to create additional basic units by plant category as authorized by section 2(b)(1) of these Crop Provisions, your SV for the purpose of establishing the amount of insurance is the sum of the SVs you established for each plant category; and

- You may be required at time of inspection to provide inventory records or comprehensive business plan to support the maximum values reported.

- For CAT coverage, your SV for each insured practice cannot exceed the lesser of:

- 110 percent of the maximum value for all the plant categories in any given month during any of the preceding three crop years; or

- The maximum of the monthly values reported on the MUVP. At the time of an inspection or at any time upon our request, you must provide inventory records to support the monthly values reported.

Q. The current nursery program allows for two upward revisions for each basic unit during a crop year. Does NVS allow for similar revisions?

Yes. You may increase your SV for each basic unit no more than twice during the crop year by submitting a revised NVR.

Q. How and where do I purchase NVS insurance?

NVS is available for purchase from your local crop insurance agent. You can find a crop insurance agent at the following link on the Risk Management Agency (RMA) website: www.rma.usda.gov/Information-Tools/Agent-Locator-Page.

These agents work for AIPs that have reinsurance agreements with the RMA.

Q. What information do I need to provide if I have a loss?

If you suspect you have a loss, you must:

- First protect the plants from further damage by providing sufficient care;

- Then notify your insurance company within 72 hours of initial discovery of damage (but not later than 15 days after the end of the insurance period); and

- Cooperate with the insurance company in the settlement of claim.

In order to complete a settlement of claim, the insurance company will need the following information:

- Documentation that supports your NVR and inventory immediately prior to the loss occurrence.

- Required documentation includes, but is not limited to, the following:

- A detailed plant list that includes the full name of each specific plant;

- Acceptable sales records for any specific plants that were sold the previous 60 days or 12 months, as applicable, that support the determination of approved sales value for each specific plant as described in section 1; and

- Documentation or demonstrated performance of your ability to properly obtain and maintain nursery plants.

- Required documentation includes, but is not limited to, the following:

- You must maintain an inventory. If requested, you must provide:

- Your most recent inventory; and

- Purchase and sales records from the date of your most recent inventory to the date of loss occurrence

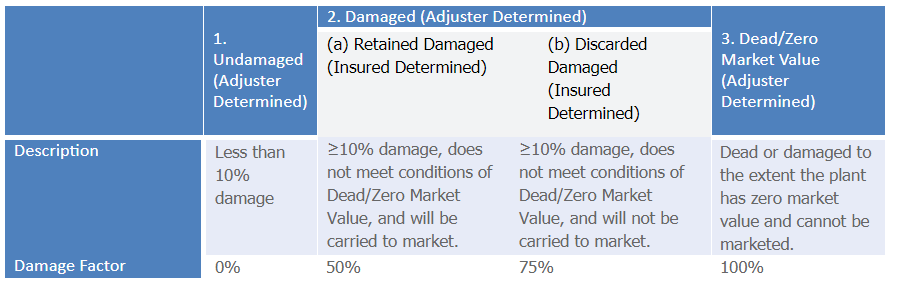

Q. Under the current nursery program, one concern is with the subjectivity of the loss adjustment process. How does NVS address this concern?

NVS addresses this concern by establishing clearly-defined criteria. Those criteria are split between two groups: 1) Liner and Annual Plants plant categories, and 2) all other plant categories. Losses are determined through a collaborative effort between the adjuster and you. In some cases, a third-party expert may need to be called in for additional guidance.

For Liner and Annual Plants plant categories, refer to the following:

For all other plant categories, refer to the following:

You must destroy or dispose of discarded damaged and dead/zero market value plants by a method approved by the insurance company.

Q. How are losses determined?

In order to determine the loss, the loss adjuster needs to know the pre-loss actual unit value and the post-loss damage value.

- The pre-loss actual unit value is the total dollar value of all insurable specific plants in a basic unit, immediately prior to the occurrence of the loss event, determined by multiplying the approved sales value by the number of each specific plant and summing the results. Pre-loss actual unit value is synonymous with field market value A under the current nursery program.

- The post-loss damage value is the total dollar value lost in a basic unit due to an insured cause of loss determined in section 12 using FCIC approved procedures and the damage factors contained in the Special Provisions. Post-loss damage value is different than field market value B under the current nursery program in that post-loss damage value is the amount of damage to the plants, whereas field market value B is the value remaining after damage occurred.

Once the loss adjuster knows those two values, the loss adjuster determines the percent of loss by dividing the post-loss damage value by the pre-loss actual unit value.

The percent of loss is then multiplied by the lesser of the pre-loss actual unit value or the SV to arrive at the value of the loss.

The indemnity is then calculated by multiplying your share by the difference between the loss and the occurrence deductible.

Q. What options and endorsements are available for NVS?

The only option available for NVS is a new Occurrence Loss Option (OLO). The OLO eliminates the unit deductible and pays a loss when the percent of loss exceeds 10 percent. The OLO is available for an additional premium, and it is only available for buy up policies.