The 2019 Outlook for U.S. Agriculture From USDA’s Chief Economist

Speaking on Thursday at USDA’s Agricultural Outlook Forum in Arlington, Virginia, USDA Chief Economist Robert C. Johansson provided a broad outlook for U.S. agriculture. Today’s update provides an overview of key aspects of Dr. Johansson’s presentation.

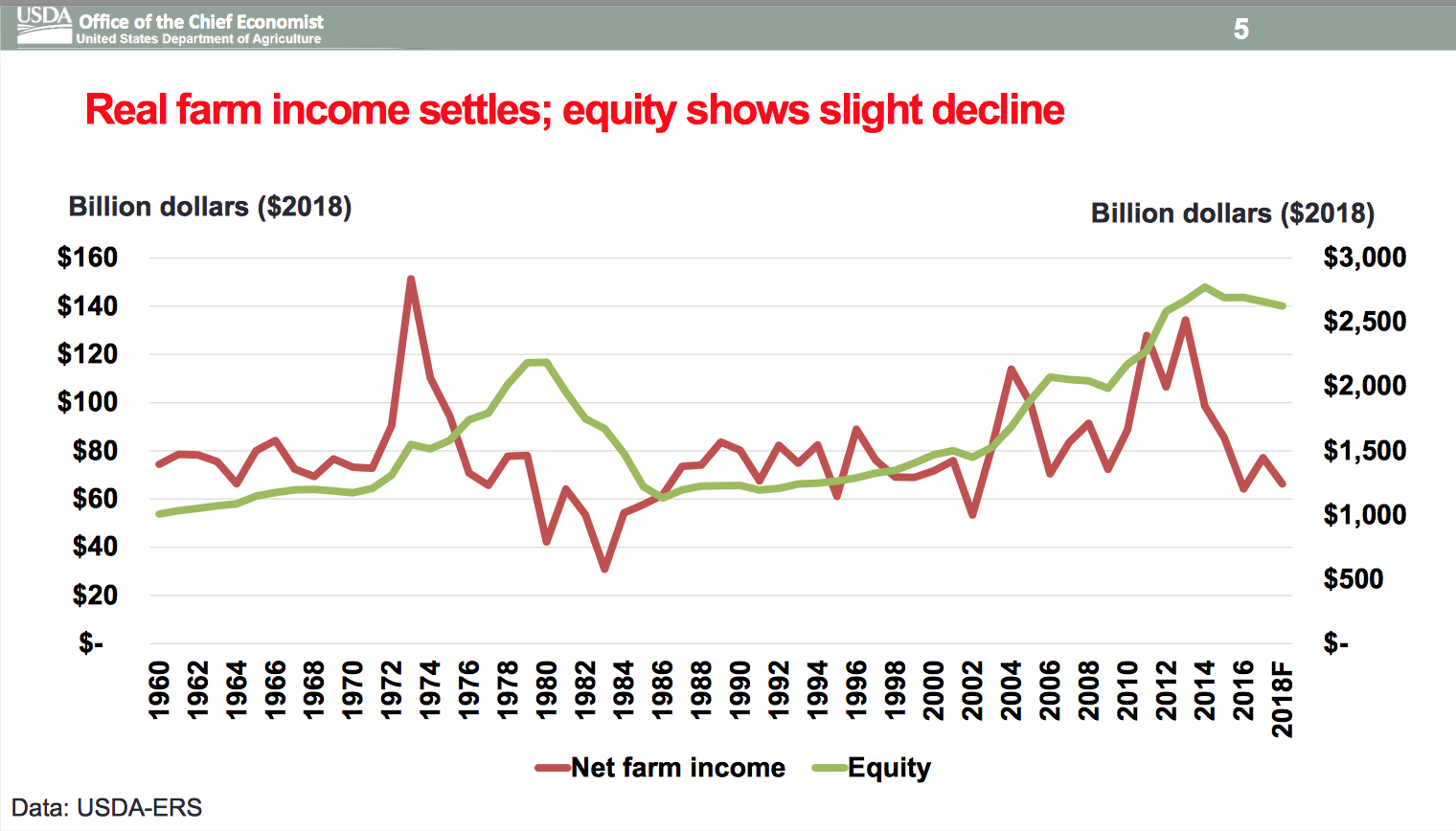

In his speech Thursday (transcript / slides), Dr. Johansson noted that, “A growing U.S. economy helps farm household income, but falling commodity prices in recent years for a host of reasons have weighed on farm income. Over the past couple of years the dramatic fall in net farm income in 2015 and 2016 seems to be leveling out at a lower level.

“The Outlook for U.S. Agriculture – 2019: Growing Locally, Selling Globally,” USDA Chief Economist Robert Johansson, February 2019.

“The current expectation of farm income at $66 billion in 2018 is a long way from the heights we saw when real net farm income peaked at $134 billion in 2013. Relative to the 10-year average, real net farm income is down 28 percent. Looking forward, net farm income is expected to rise slightly, remaining below $80 billion annually over the next 10 years.”

Dept. of Agriculture

✔@USDA

USDA Chief Economist Rob Johansson takes the stage to provide the 2019 Agricultural Economic & Foreign Trade Outlook #AgOutlook #OATT

“The Outlook for U.S. Agriculture – 2019: Growing Locally, Selling Globally,” USDA Chief Economist Robert Johansson, February 2019.

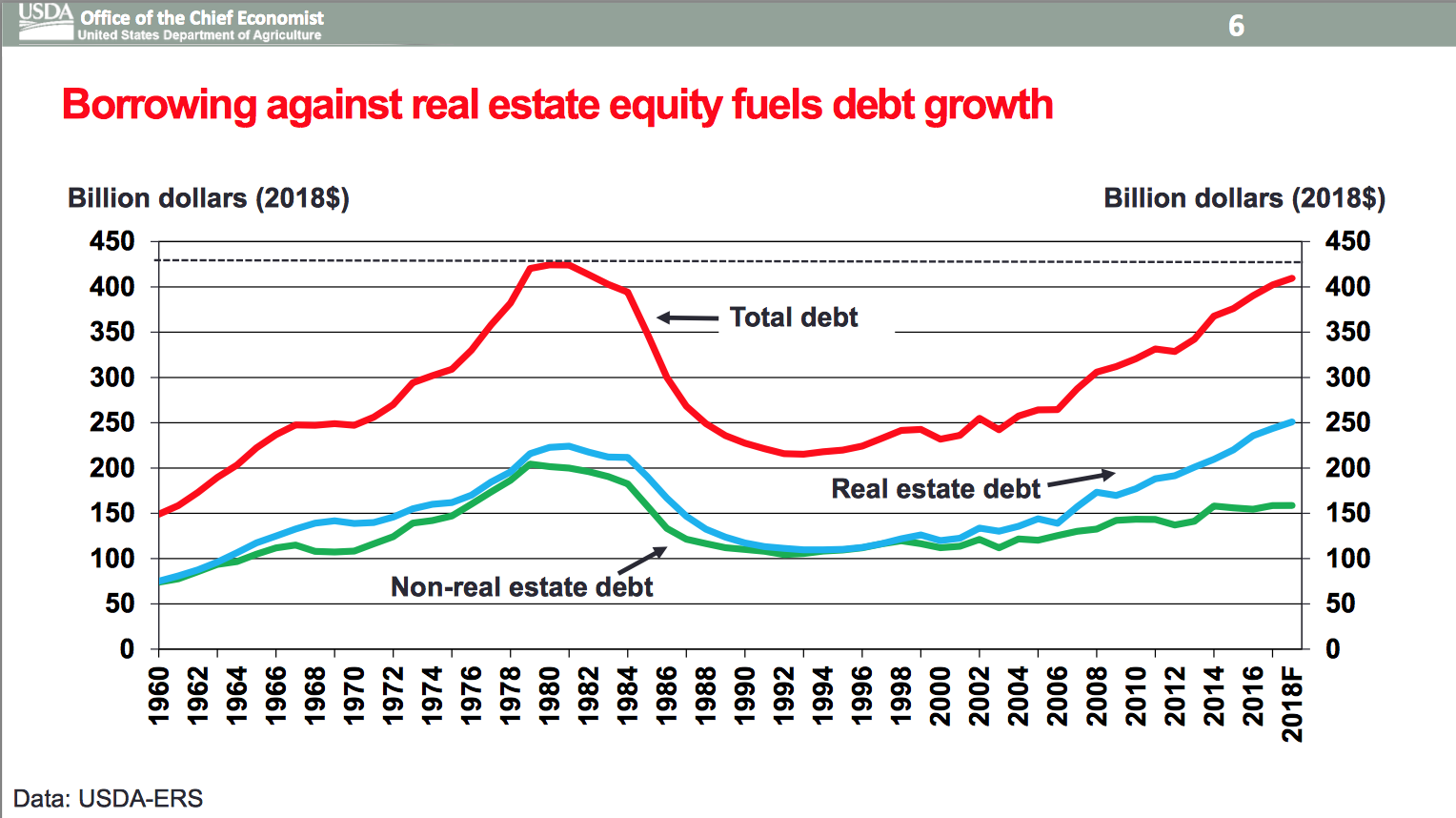

“With low commodity prices, farmers have increasingly tapped into their real estate equity to provide operating funds. Today, total debt is approaching record levels in real terms, and real estate debt has reached a record high in 2018.”

While still a long way from the peak of 60 percent in 1983, the growing share of farmers’ crop andlivestock cash receipts that goes towards financing debt is likely to cause cash-flow problems for producers without significant land equity.

Turning to address the U.S. crop forecast, Dr. Johansson stated that, “Our general expectation is for continued declines in real agricultural commodity prices over the next 10 years. Falling commodity prices are the result of continued production growth, which continues to outpace global demand.”

More narrowly, with respect to soybeans, Dr. Johansson pointed out that, “While U.S. soybean prices have been slightly buoyed amid some signs of progress in negotiations, the export outlook for this year’s crop (2018/19) remains challenging. Currently, the U.S. has exported 24 million metric tons of soybean, down 13.5 million metric tons from this time last year. Under the trade dispute, exports to China alone have plummeted by 22 million metric tons, or over 90 percent.”

The record high [soybean] stocks in the U.S. due to the trade situation will take several years to unwind, which will weigh on U.S. prices going forward even with potential China purchase agreements. Compared to our 10-year projection of soybean prices from last year, our current estimates show that prices for soybeans are likely to take at least until the 2020 crop year to recover.

“The Outlook for U.S. Agriculture – 2019: Growing Locally, Selling Globally,” USDA Chief Economist Robert Johansson, February 2019.

With respect to prices, Dr. Johansson noted that, “Under the expectation of continued Chinese tariffs, soybean prices are expected to rise modestly, up $0.20 to $8.80 per bushel as the market begins the multi-year process of working down large stocks, but this follows the prior year’s decline of $0.73 per bushel. Alternatively, corn is expected up $0.05 to $3.65 per bushel, but is a second year of price increases as carry out stocks are expected to continue their multi-year tightening.”

“The Outlook for U.S. Agriculture – 2019: Growing Locally, Selling Globally,” USDA Chief Economist Robert Johansson, February 2019.

“With the large overhang in soybean stocks, soybean area needs to adjust to work down record large soybean carry-in stocks. As a result, soybean area is expected to fall 4.2 million acres, to 85 million acres in 2019.”

“The Outlook for U.S. Agriculture – 2019: Growing Locally, Selling Globally,” USDA Chief Economist Robert Johansson, February 2019.

While addressing trade issues in more detail, Dr. Johansson indicated that, “Overall, U.S. agricultural exports are currently forecast at $141.5 billion in fiscal 2019, down $1.9 billion from 2018. The share of total U.S. agricultural exports to China in value terms is projected to be 6 percent, down sharply, with China falling from the top market in 2017 to fifth place.”

“The Outlook for U.S. Agriculture – 2019: Growing Locally, Selling Globally,” USDA Chief Economist Robert Johansson, February 2019.

After additional remarks on trade and U.S. farm policy variables, the USDA’s Chief Economist pointed out that, “On December 20th, President Trump signed the Agriculture Improvement Act of 2018. The new Farm Bill is expected to cost approximately $428 billion over 5 years, slightly higher than the cost of continuing the 2014 Farm Bill.”

“The Outlook for U.S. Agriculture – 2019: Growing Locally, Selling Globally,” USDA Chief Economist Robert Johansson, February 2019.

“U.S. farm policies have evolved over time, moving from reliance on programs that controlled how much and what producers could plant (i.e., the ‘coupled’ programs in slide 31 above) to an array of programs that give producers the chance to make decisions based on market signals and their own risk management preferences.”